By Phil Ganz

By Phil Ganz

Edited by Ryan Skerritt

Edited by Ryan Skerritt

One key highlight of these updates is the focus on Accessory Dwelling Units (ADUs), more minor, secondary housing units on a residential property. The main point of this article is to explain how the new FHA guidelines now allow you to include rental income from an ADU when qualifying for a mortgage.

This change has the potential to make homeownership more attainable for many people. So, let's dive in to understand what these changes mean and how they could benefit you.

Major FHA Guidelines Changes

The Mortgagee Letter 2023-17, released by the Federal Housing Administration (FHA), introduces several important updates that affect borrowers, property owners, and industry professionals.

Here are the fundamental changes outlined in the letter:

-

Inclusion of ADU Rental Income in Effective Income for Borrowers - The new guidelines allow for the inclusion of rental income generated from an Accessory Dwelling Unit (ADU) in a borrower's Effective Income. This is to qualify for an FHA-insured mortgage.

-

Updated Property Eligibility Guidelines - The letter updates what types of properties are eligible for FHA-insured financing, mainly focusing on those with ADUs. These properties are now included under the Standard 203(k) Rehabilitation Program and as suitable property types for new construction financing.

-

Revised Appraisal Protocols for ADUs - Appraisers are now given specific protocols for analyzing and reporting market rent for ADUs. This is essential for the FHA loan approval process.

-

Updated Reserve Requirements for Properties with ADUs - The letter outlines new reserve requirements for properties that have an ADU. These reserves are essential as they act as a financial safety net for the borrower.

-

Clarifications on Rental Income Restrictions for Cash-Out Refinances - The letter clarifies that rental income from an ADU cannot be used as Effective Income for Cash-Out Refinances. This is a specific restriction to be aware of.

-

Updates to Types of Eligible Improvements under the Standard 203(k) Program - The guidelines now provide more detail on what types of improvements to an ADU are eligible under the Standard 203(k) Rehabilitation Program.

- Additional Guidance on HECM Financial Assessment and Property Charge Guide - The letter includes new guidance related to rental income and ADUs in the Home Equity Conversion Mortgage (HECM) Financial Assessment and Property Charge Guide.

Each of these changes aims to offer more clarity and flexibility to borrowers, helping them better understand how ADUs can be leveraged in applying for an FHA-insured mortgage.

These updates are effective immediately and will be included in the forthcoming update of the HUD Handbook 4000.1.

What are ADUs?

Accessory Dwelling Units, or ADUs, are independent living spaces located within or on the same property as a single-family home. They can be basement apartments, over-garage studios, or backyard cottages, offering supplemental rental income possibilities to homeowners.

For real estate investors, ADUs provide an opportunity to increase return on investment. They can enhance property value, appeal to prospective buyers or tenants seeking multi-generational living options, and offer affordability in high-cost housing markets.

Definition of ADUs

An Accessory Dwelling Unit (ADU) is a self-contained living space offering all the essentials of a traditional house - a kitchen, bathroom, and sleeping area. It can be integrated into the existing structure or built as a detached unit.

Accessory Dwelling Units (ADUs) enhance property value and provide the potential for rental income, making them a profitable addition to real estate investments.

ADUs, colloquially known as 'granny flats' or 'in-law suites,' are typically constructed in a primary residence's backyard, garage, or basement. This layout offers occupants independent living while still within a stone's throw of the main house.

Potential homebuyers intending to purchase properties with ADUs must grasp their precise structure. Multiple configurations exist, ranging from converted garages and basements to standalone cottages or an apartment over a garage.

Understanding this structure is essential because the type of ADU can significantly impact its rental income potential, maintenance costs, and overall market value of the property. Therefore, prospective homebuyers should consider ADUs beneficial additions to their real estate portfolio.

Benefits of ADUs for Homeowners

ADUs, or accessory dwelling units, provide immense value to homeownership. It extends beyond the primary offering of additional living space to substantial financial benefits and an enhanced property value.

-

ADUs can serve as a source of regular rental income, financially empowering homeowners.

-

Adding an ADU can significantly augment the home's overall market value.

-

ADUs can act as supplementary living spaces for family members or for home-based business purposes.

-

In fluctuating home prices, stable rental income from ADUs can provide financial security.

- ADUs can be instrumental in responsible property investment for potential real estate investors.

Understanding the New FHA Guidelines

The new FHA guidelines provide an essential roadmap for home buyers and real estate investors, shedding light on how rental income from ADUs can be utilized to qualify for a mortgage. They expand the realm of opportunities but also demand a strategic approach.

A comprehensive review of the updated FHA guidelines reveals explicit stipulations on rental income's role in mortgage qualification. Understanding the impact of these changes is paramount for homeowners and investors looking to maximize their ADUs' potential.

As the FHA guidelines evolve, so must your understanding of how to harness ADUs to meet your mortgage needs. These changes offer challenges and opportunities, requiring detailed comprehension for successful navigation.

Overview of FHA Guidelines on Rental Income

Recent changes to Federal Housing Administration (FHA) guidelines stipulate that rental income from accessory dwelling units (ADUs) can be calculated for mortgage qualification. This update simplifies securing a mortgage, making homeownership more accessible.

The critical element of these revised guidelines is the allowance of rental income from ADUs. Previously, it took a lot of work for homeowners to document this supplementary source of income effectively.

New FHA guidelines recognize income from ADUs and provide a step-by-step guide to improve rental payments. This includes allowing homeowners to use prospective rental income to qualify for bigger loans.

For homeowners, this shift in policy could mean a substantial rise in eligible borrowing power. The boost in rental income calculations transforms ADUs into valuable assets, improving borrowing capacity and property investment potential.

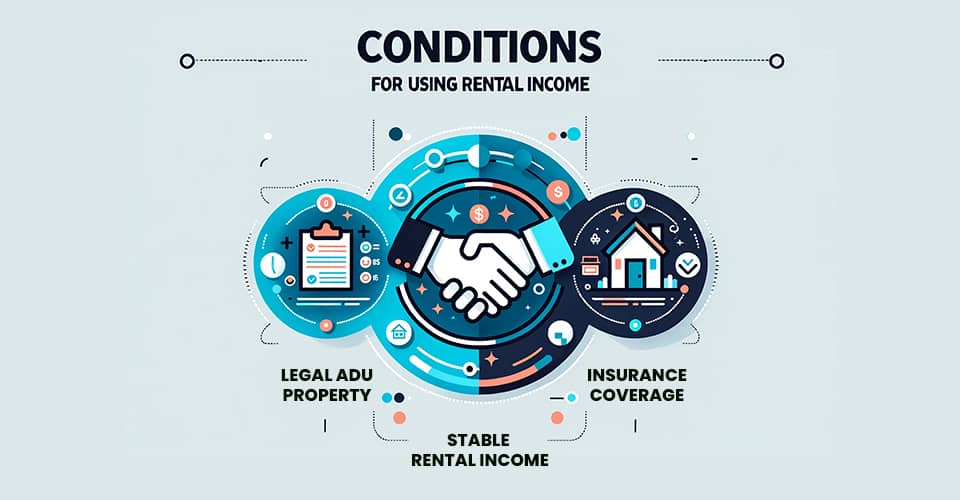

Critical Requirements for Using Rental Income from ADUs

The FHA stipulates crucial conditions for potential homeowners to apply rental income from ADUs towards mortgages. Navigating these prerequisites is essential to know if your ADU rental income can aid in mortgage qualification.

-

Accurate documentation of a stable rental income history for the ADU.

-

Legal ADU property as per local zoning laws.

-

Adequate insurance coverage, including landlord liability.

-

The buyer must occupy the main home as their principal residence.

- Appraisal report evidence of ADU's marketability as a rental property.

Qualifying for a Mortgage with Rental Income from ADUs

Rental income from Accessory Dwelling Units (ADUs) can be a game-changer in unlocking mortgage eligibility for many homeowners and potential buyers. This income stream bolsters your earning capacity and strengthens your mortgage application.

Leveraging the rental income from an ADU can act as a stepping stone for qualifying for a larger mortgage. It provides an opportunity to demonstrate consistent income, providing a solid foundation for mortgage approval.

Calculating Rental Income from ADUs

When calculating rental income from ADUs, lenders consider various factors to ascertain the stability and reliability of your rental earnings.

-

Analyzing lease agreements or a history of rental income documented on tax returns.

-

Estimation of potential rental income as supported by a rent survey conducted by an approved appraiser.

- The individual lender's policy governs calculation methodologies.

Debt-to-Income Ratio Considerations

When leveraging ADU rental income for mortgage qualification, the debt-to-income (DTI) ratio plays a significant role.

It's crucial to understand that lenders use this ratio to determine your ability to manage your monthly debt payments and how the additional income from the ADU impacts this ratio.

-

Identify all your monthly debt liabilities.

-

Calculate total monthly income, including the potential ADU rental income.

-

Determine the total debt-to-income ratio.

-

Analyze how the additional payment from the ADU affects the DTI ratio.

- Ensure that even with the ADU income factored in, the DTI remains within the FHA guidelines.

Verification of Rental Income

Rental income verification is pivotal in the context of ADUs. It supports a borrower's capacity to repay and affects the final loan amount pre-approval.

Mortgage lenders require proof of steady rental income before approving a loan. In the case of ADUs, it can be documented lease agreements or a reliable record of payment receipts.

It's important to remember that unverified rental income from ADUs is unlikely to be considered in the mortgage qualifying process. Lenders seek concrete proof of dependable future cash flow.

Therefore, the rental income from ADUs has identified itself as a cornerstone of mortgage qualification. Confirmed and steady rental income can help secure better loan terms.

Tips for Maximizing Rental Income Potential

By capitalizing on the new FHA guidelines, homeowners can strategically utilize rental income from ADUs to meet mortgage qualification criteria. This financial windfall can significantly enhance your borrowing capabilities when reflected appropriately in your debt-to-income ratio.

To further boost your rental revenues, consider the optimal use of ADU space, attract high-quality tenants, and set competitive rental prices following a detailed market analysis. Enhanced rental income can thus facilitate the approval of a higher mortgage amount.

Optimizing ADUs for Higher Rental Income

Strategies recommended by FHA guidelines to increase your ADU's rental appeal include modernizing the interior, offering competitive amenities, and maintaining a well-kept and attractive exterior. Properly managed ADUs can significantly enhance your property's overall rental income.

Maximizing your real estate investment returns under the new FHA guidelines requires a smart ADU optimization strategy. Explore potential upgrades like energy-efficient appliances or high-speed internet - amenities attractive to tenants.

A thorough understanding of FHA regulations and a focus on improving your ADU's tenant appeal can offer a competitive edge. Choose improvements that boost property value and align with potential renters' preferences.

Attracting Quality Tenants

A reliable tenant plays a crucial role in maintaining your ADU's value, and the FHA guidelines may assist with this. These rules factor in the viability of rental income, making your property more attractive to prospective tenants.

Did you know you could tailor your ADU to attract reliable tenants? Focused improvements, in line with FHA standards, can enhance appeal and rentability.

The new FHA guidelines favor properties that have legal, income-producing ADUs. This implies a steady flow of responsible tenants, providing landlords more confidence and stability.

An FHA-compliant ADU ensures potential rental income and increases property visibility. It's akin to a tenant magnet, attracting those who value regulated, upfront housing solutions.

You build a solid track record with tenants by maintaining your ADU by the FHA guidelines. This not only attracts high-quality renters but also increases tenant retention.

Market Analysis and Rental Pricing

Determining the right rental price for your ADU under the new FHA guidelines is crucial. Conduct market analyses to understand average rates, ensuring your price is competitive yet profitable.

Consider your property's unique features and location when setting the rental price. Premium property characteristics may warrant a higher rental price, giving an edge in loan qualification.

Pay attention to the role of seasonal market trends in rental pricing. Timing is pivotal; understanding peak rental seasons can maximize rental income and your mortgage qualification prospects.

The new FHA guidelines recommend frequent reviews of your ADU rental pricing strategy. This helps keep pace with an ever-evolving real estate market, enhancing loan qualification chances.

Considerations for Real Estate Investors

Understanding the new FHA guidelines relating to ADUs can significantly empower real estate investors. By leveraging the rental income from ADUs, investors can easily navigate mortgage qualifications and benefit from the potential for steady cash flow.

The evolving landscape of real estate investment is inescapable, and with the introduction of the new FHA guidelines, taking advantage of opportunities presented by ADU rental income becomes even more appealing. Ensure you grasp these opportunities while being well-informed to optimize your investment returns.

ROI Analysis for ADU Investments

Quantifying the ROI of your ADU investment provides essential insights into the financial gains attributable to the new FHA guidelines. By accounting for rental income considerations in their mortgage qualification standards, FHA has substantially increased the value proposition of investing in ADUs.

Understanding how ADU rental income affects your mortgage eligibility requires an ROI analysis comprising rental income, mortgage payments, and potential ADU-related expenses. A higher ROI indicates a profitable investment and enhances your mortgage qualification prospects per the revised FHA guidelines.

Legal and Regulatory Considerations

As ADUs become more popular, new FHA guidelines reshape the regulatory dynamics of ADU investments, adding potential advantages for homeowners and investors. Alterations in rental income acknowledgment broaden investment opportunities and change the legal landscape for property holders.

Legalities around using ADU rental income for mortgage qualification have evolved alongside FHA guidelines. Potential homeowners must acquaint themselves with these changes to maximize the benefits while ensuring legal compliance.

The FHA's updated rules provide a fresh perspective on ADU investments. Investment decisions need to incorporate the legal aspects that hinge on these changes, thus ensuring that property owners navigate the path to mortgage qualification efficiently and legally.

Property Management and Maintenance

Implementing a strategic approach to ADU maintenance under the new FHA guidelines proves beneficial. Good maintenance habits enhance the property's value and uphold its eligibility for FHA-backed loans. It's essential to consider short- and long-term maintenance needs to support loan qualification.

Quality property management practices directly affect rental income from ADUs. Under the new FHA guidelines, having a solid property management strategy demonstrates your rental income's sustainability. This, in turn, can influence your mortgage qualification.

Neglecting property maintenance can negatively affect your chances of qualifying for a mortgage. Factors such as the property's condition, regularity of repairs, and adherence to building codes are crucial in adhering to FHA guidelines.

Efficient property management extends beyond maintenance—it encompasses tenant relations as well. Timely repairs and updates enhance tenant satisfaction, leading to long-term occupancy and steady rental income. Such consistency can help meet FHA's rental income stipulations.

Emphasize regular inspections and preventative maintenance to reduce sudden, expensive repair needs. The aim is to manage costs and maintain rental viability. When documented well, such an approach could positively impact your FHA loan qualification.

Exit Strategies and Potential Risks

Investors must consider potential risks and form coherent exit strategies for their ADU investments. While rental income from ADUs can significantly aid in mortgage qualification, planning for scenarios like regulatory changes, vacancies, or market downturns is critical.

Savvy investors understand that every investment carries risk. Leveraging ADU rental income for a mortgage is no exception. Potential risks may include but are not limited to higher maintenance costs, rental market fluctuation, and legislative changes affecting ADUs. Thus, forming a risk mitigation and exit strategy in advance is paramount.

With over 50 years of mortgage industry experience, we are here to help you achieve the American dream of owning a home. We strive to provide the best education before, during, and after you buy a home. Our advice is based on experience with Phil Ganz and Team closing over One billion dollars and helping countless families.

About Author - Phil Ganz

Phil Ganz has over 20+ years of experience in the residential financing space. With over a billion dollars of funded loans, Phil helps homebuyers configure the perfect mortgage plan. Whether it's your first home, a complex multiple-property purchase, or anything in between, Phil has the experience to help you achieve your goals.

About Editor - Ryan Skerritt

Ryan Skerritt has over 10+ years of experience in the residential financing space. With over two hundred and fifty million of funded loan volume, Ryan has the skill set to help any homebuyer configure the perfect mortgage plan.